Current inflation readings are trending lower and the Federal Reserve is lowering interest rates. Market sentiment improved dramatically during the quarter as trade-war fears eased and attention shifted to government stimulus (via the hotly debated “One Big Beautiful Bill”) and lower interest rates. Portfolio performance was led by our “Big Tech” and Health Care Provider investments which more than offset temporary weakness in our Housing and Health Care Payer investments. I am pleased by the first-half performance which demonstrated capital preservation and appreciation during a very volatile period. I believe our active management approach of avoiding froth and allocating to significantly discounted, market-leading franchises positions us well for strong risk-adjusted investment returns.

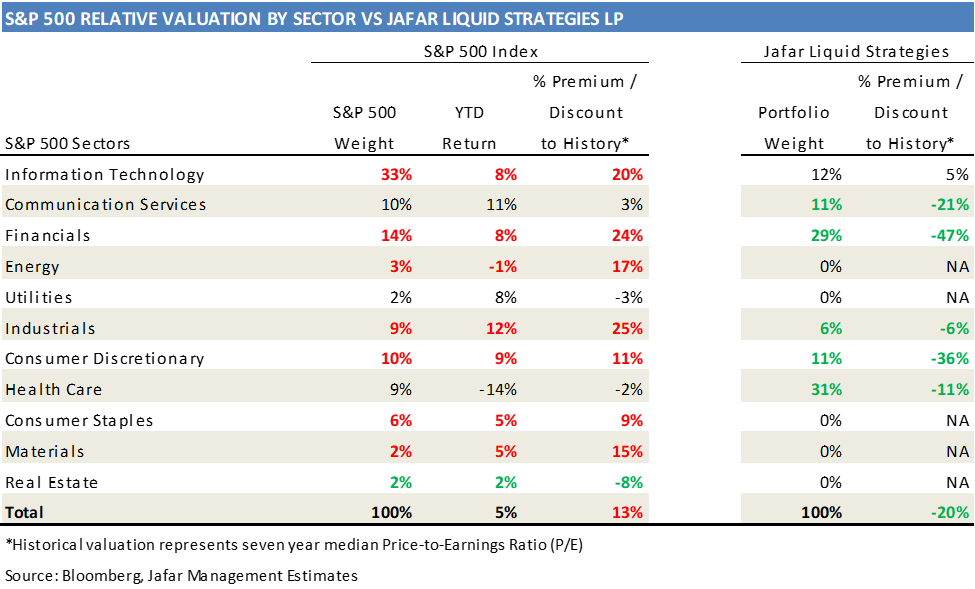

Greed and exuberance have returned as the market has chased the most volatile sectors at the expense of sectors traditionally considered conservative. The table below shows how the year-to-date market returns have been driven by the most volatile sectors becoming more expensive while the lower-volatility sectors have gotten cheaper. In total, the S&P trades at a +13% premium while our portfolio trades at a -20% discount to historical valuations as we have proactively rotated out of expensive areas and allocated to investments that I believe offer significantly better future return profiles and valuation.

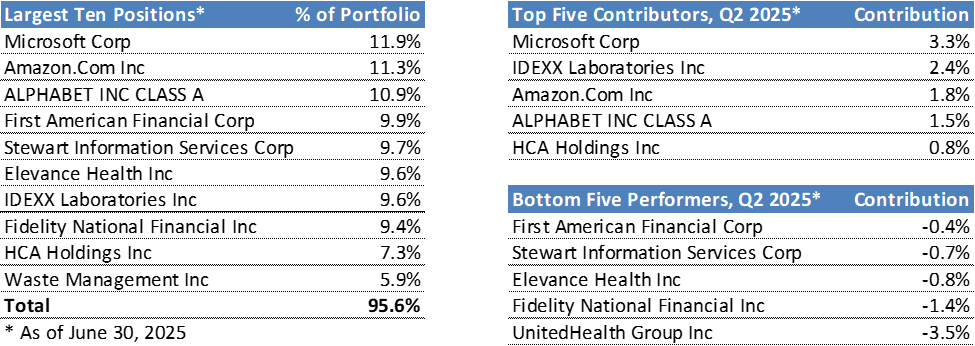

Portfolio Update

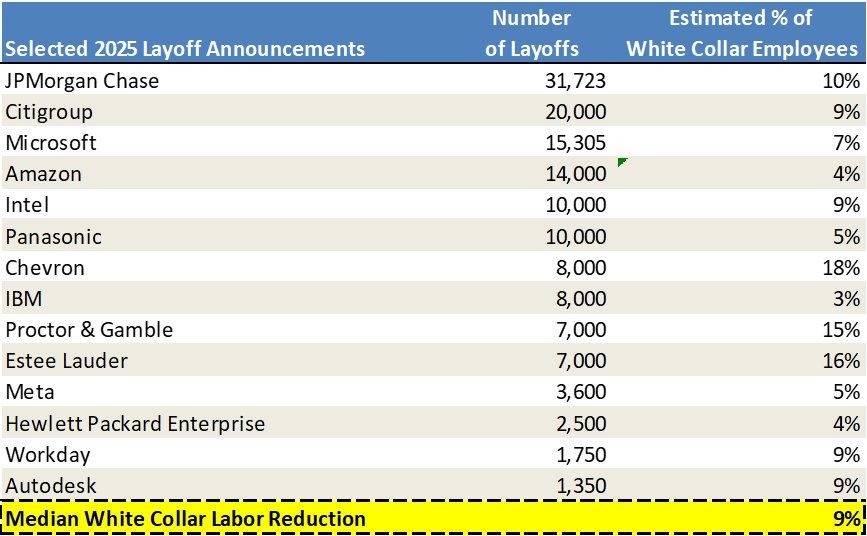

Owning high-quality oligopoly/monopolistic businesses is a core tenet of our strategy that I believe will deliver strong results over the long-term. Each investment is expected to generate multiples-of-money (minimum 15% IRR) on a standalone basis, however, I believe we are currently at the early stages of a transformational moment that will significantly amplify the return profile of our investments. I expect the value creation from Artificial Intelligence will accrue to companies that fit our strict investment criteria, importantly: dominant companies in growing industries with strong pricing power. We are now seeing the adoption of this technology and the impact to white-collar payrolls. Some recent quotes from corporate executives carry a powerful message:

- “As we roll out more Generative AI and agents, it should change the way our work is done. We will need fewer people doing some of the jobs that are being done today, and more people doing other types of jobs. It’s hard to know exactly where this nets out over time, but in the next few years, we expect that this will reduce our total corporate workforce as we get efficiency gains from using AI extensively across the company.” – Andrew Jassy, CEO of Amazon (June 2025)

- “Your children are going to live to 100 and not have cancer because of technology, and literally they’ll probably be working 3.5 days a week” – Jamie Dimon, CEO of JPMorgan (November 2024)

- “Before asking for more Headcount and resources, teams must demonstrate why they cannot get what they want done using A.I.” – Tobi Lutke, CEO of Shopify (April 2025)

The table below is just a small sample of companies that have announced labor reductions in 2025:

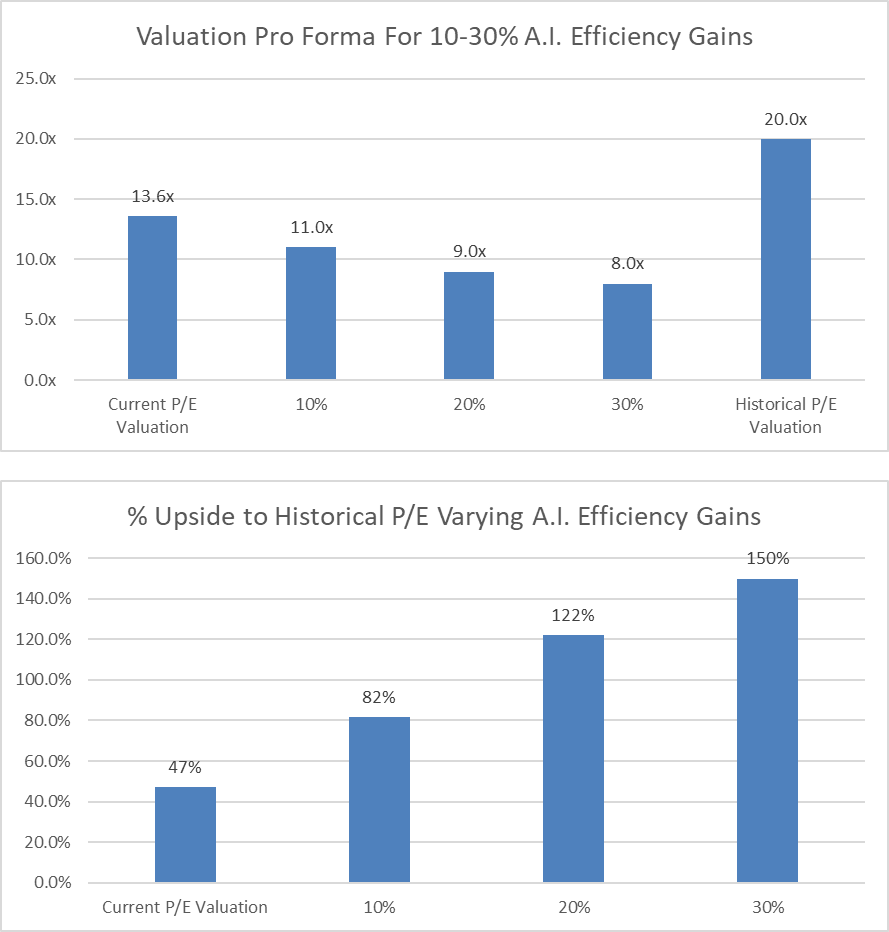

Our allocations to sectors outside of Technology represent 66% of our portfolio and have large white-collar labor forces. The tables below illustrate the deep discount embedded in these portfolio investments today and the amplified upside potential assuming Artificial Intelligence generates efficiencies in the white-collar labor force. As we have actively managed our allocations away from the frothiest pockets of the market, our non-tech investments could see +47% upside as their valuations normalize to historical levels (just marking-to-market, not including any benefit from future earnings growth). In the event A.I. efficiency gains materialize, the return potential jumps to +82-150%.

On a consolidated basis, our portfolio of diverse, dominant, and resilient franchises offers an attractive 5.4% earnings yield, 1.7% dividend yield and beta of 0.8. Considering these factors, I believe the expected return profile of our partnership is very exciting and is significantly more favorable than alternative investment opportunities. My family balance sheet remains fully invested with you and I am excited about our future. Thank you for your trust and please feel free to reach out anytime.