Many of last year’s stock market laggards are rebounding as inflation, interest rates and currency headwinds abate. The real economic impacts of the interest rate hiking cycle have become more pronounced as demonstrated by the widely publicized bank failures. While news headlines of bank failures can certainly provoke one’s anxiety, ironically, there are reasons to be optimistic:

- The banking crisis is a product of the Federal Reserve’s aggressive interest rate hikes to combat inflation. Banks were caught offsides as their assets declined in value while depositors emptied their accounts to earn yield on their cash elsewhere. Inflation was showing signs of cooling before the bank failures occurred and a weakened banking sector will likely have a deflationary effect via fewer loans for client investment/spending, and the wealth destruction felt by those who invested in banks. Importantly, the government has gone to great lengths to protect depositors which in turn protects the banking system. Ultimately, the quicker inflation subsides, the faster the Federal Reserve will lower rates which can alleviate some of the pressures on banks.

- There is little doubt that the economy faces near-term headwinds, however, today’s economic headwinds can quickly become yesterday’s news (i.e. the markets are forward looking). If inflation continues to cool and the Federal Reserve responds with lower interest rates, the markets will likely shake off the (Fed induced) difficulties of 2023 and look to the brighter days of 2024/beyond.

Portfolio Update

Last quarter I outlined the tools at our disposal to address the volatility the portfolio experienced last year. I am pleased to report that we have made significant progress and we are seeing early signs of these actions bearing fruit. The tables below show our largest allocations, some of which remain our core holdings in the themes of eCommerce, Enterprise Computing and some are new allocations in market leading franchises with very exciting investment potential. The highlights below are examples of how I am thinking about the investment potential of our portfolio companies (both old and new investments).

Amazon

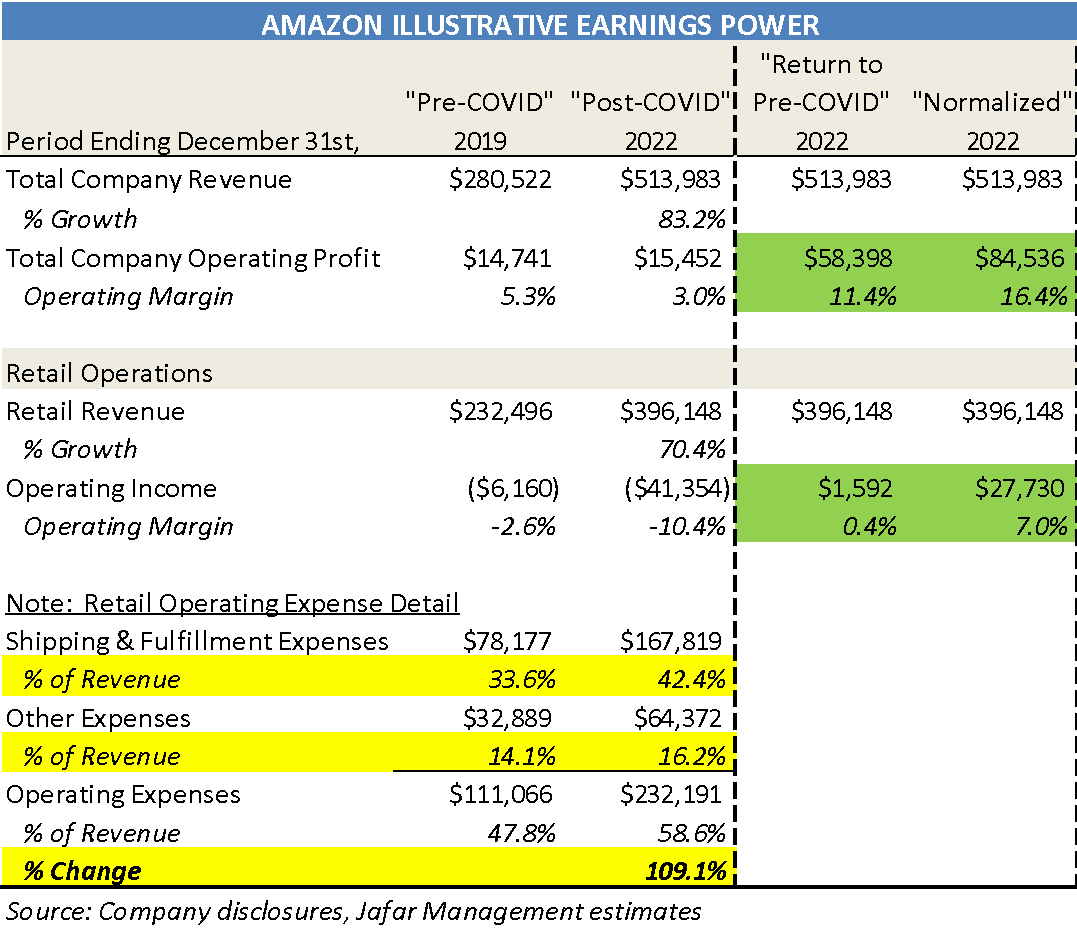

Amazon has been a core holding in our collection of eCommerce and Enterprise Computing investments. In 2022, the company generated $514 billion of revenue which was +83% higher than revenue generated in 2019 (“Pre-COVID”). To meet the surging customer demand during the COVID period, the Company doubled its eCommerce retail infrastructure in just two years. Per the table below, I estimate this inefficient expansion temporarily weighed on the Company’s operating profits which are understated by a magnitude of ~$43-$69 billion (+275%-445% vs 2022 reported Operating Income!).

Chief Executive Officer Andy Jassy recently published Amazon’s annual letter to shareholders which shed light on this dynamic and efforts to drive more cost efficiency:

“During the early part of the pandemic, with many physical stores shut down, our consumer business grew at an extraordinary clip, with annual revenue increasing from $245B in 2019 to $434B in 2022. This meant that we had to double the fulfillment center footprint that we’d built over the prior 25 years and substantially accelerate building a last-mile transportation network that’s now the size of UPS (along with a new sortation center network to assist with efficiency and speed when items needed to traverse long distances)—all in the span of about two years. This was no easy feat, and hundreds of thousands of Amazonians worked very hard to make this happen. However, not surprisingly, with that rate and scale of change, there was a lot of optimization needed to yield the intended productivity. Over the last several months, we’ve scrutinized every process path in our fulfillment centers and transportation network and redesigned scores of processes and mechanisms, resulting in steady productivity gains and cost reductions over the last few quarters. There’s more work to do, but we’re pleased with our trajectory and the meaningful upside in front of us.”

I am encouraged to see the early progress on cost optimization and the message from the CEO (combined with recently publicized headcount reductions) suggests we are at an inflection point for profitability improvement. Assuming the company can return to “Pre-COVID” efficiency (which still embedded high levels of spending) or more “normalized” levels of spending as benchmarked by similar companies of this scale, Amazon’s underlying 2022 earnings yield would be ~5-7%. Taking this into consideration, I believe the stock is very cheap (trading near trough valuation representing a 35% discount to the last 7 years) and has the potential to more than double as the underlying earnings power comes to light.

Waste Management

As mentioned earlier, many of last year’s outperforming stocks sold off during the first quarter as investors rotated into last year’s laggards. This dynamic created opportunities to diversify our portfolio’s sector exposures while acquiring market leading franchises at very attractive prices. I am excited to introduce our new investments in the North American Waste Collection & Disposal industry which provide essential services that generate strong, growing, resilient cash flows. These companies are traditionally viewed as stable businesses with modest volume growth and pricing power to offset inflation, however, I believe we are entering a transformational moment in the industry’s history that will structurally accelerate the earnings power for the market leaders.

Technology and government incentives are paving the way for landfill owners to harvest landfill gas (a natural byproduct of waste decomposition) and sell it as renewable energy. Waste Management is investing $1.2 billion to build 20 new facilities capable of producing gas volumes of ~28M MMBtu. The company estimates these first 20 facilities will generate an incremental $500mm of annual operating profit by 2026 with the $1.2 billion investment recouped by the end of 2026. Furthermore, the company estimates there is an additional ~48M MMBtu to develop beyond the initial 20 sites which suggests the total incremental operating profit from these endeavors exceeds +$1 billion. Waste Management recently showcased their vision and illustrated the cash flow growth they see in the chart below (please note, the chart does not include the upside from the additional ~48M MMBtu):

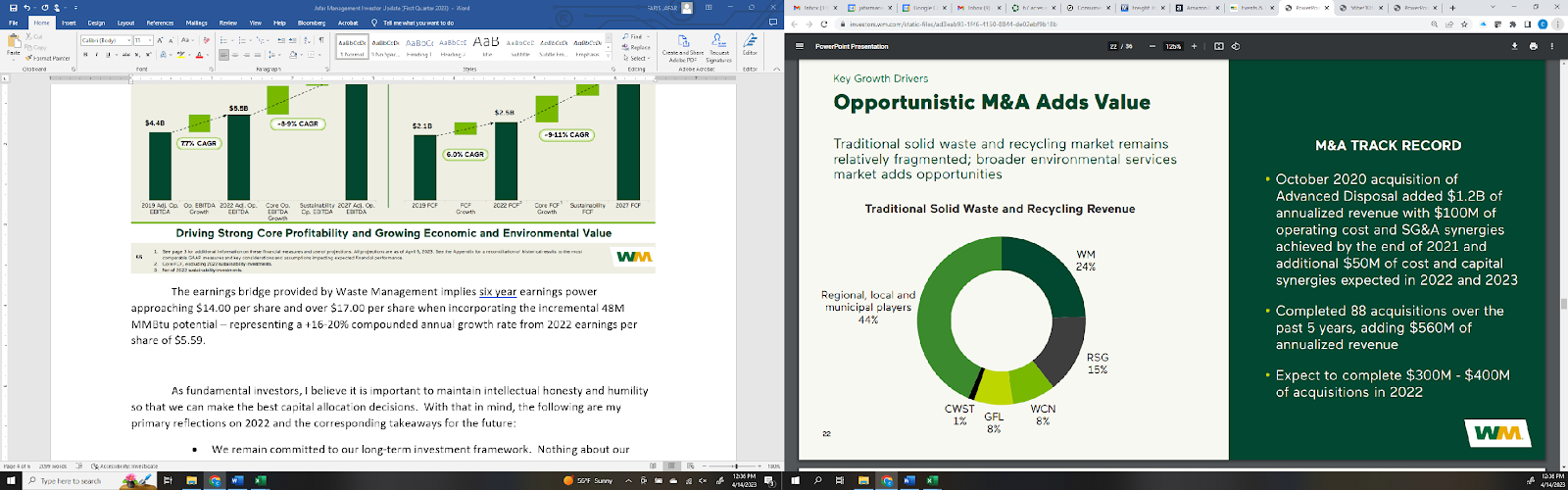

While the incremental earnings provided by these high return-on-investment landfill gas projects are attractive, I am most excited about the transformational opportunity they present. In addition to selling the energy harvested from its landfills, Waste Management has the largest heavy-duty compressed natural gas truck fleet of its kind (representing 74% of its collection routes and growing). The company’s ability to increase monetization of its existing landfills while also vertically integrating the fuel of its truck fleet create a structural advantage that smaller competitors cannot match. I believe the company (and the other top 3 leaders) can use the cash flows from the landfill gas projects to win contracts away from smaller competitors that lack the scale to implement these projects. Per the chart below, these smaller competitors represent 44% of the market, providing tremendous runway for the largest operators to take share.

The earnings bridge provided by Waste Management implies earnings power approaching $14.00 per share by 2028 and over $17.00 per share when incorporating the incremental 48M MMBtu potential – representing a +16-20% compounded annual growth rate from 2022 earnings per share of $5.59. Taking the growth and earnings power into consideration, I believe Waste Management stock has the potential to be worth over $400 per share representing multiples of money from the current price of $165.

Title Insurance

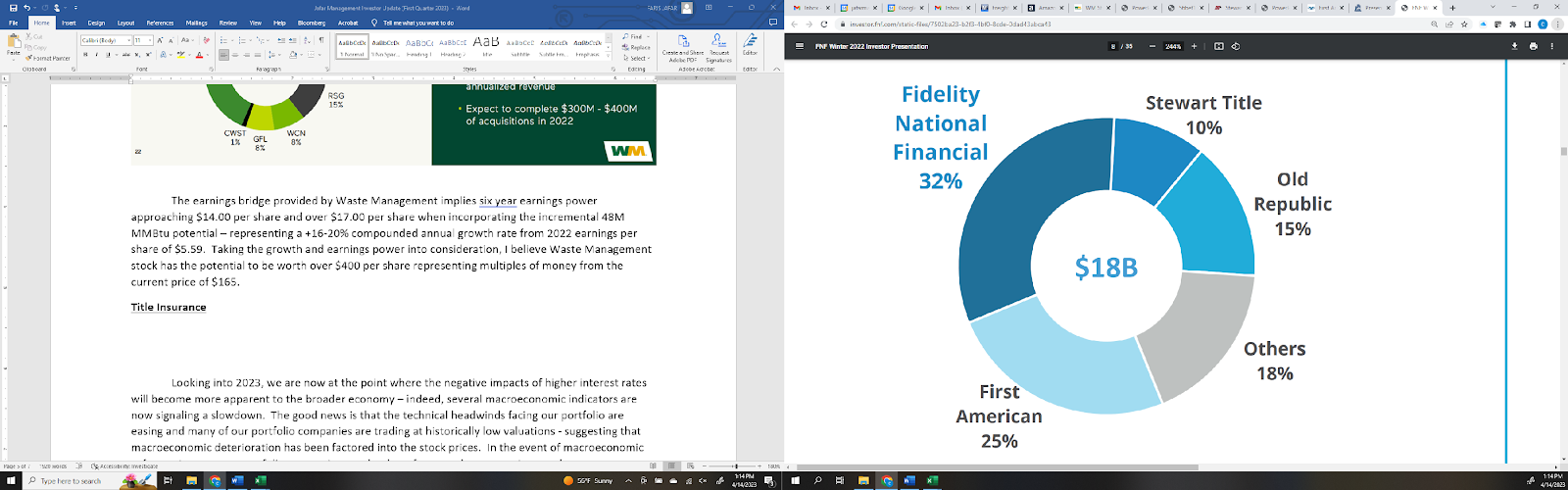

One of the most front-of-mind industries impacted by the surge in interest rates are the Residential and Commercial Real Estate industries. The Title Insurance industry provides protection against losses that occur when title to a property is not free and clear of defects (i.e. the person that sells the property is actually allowed to sell it). Furthermore, if a property purchase is financed with a mortgage, the lender will require a loan policy of title insurance which protects the lender’s interest in the property. The insurance is purchased in full at the time of the property transaction and represents ~0.5-1.0% of the purchase price. Given the low cost of the insurance relative to the protection and the policy requirement by mortgage lenders, Title Insurance is a classic example of an entrenched toll-taking business that sits on top of a critical multi-trillion dollar real estate industry. The chart below shows the market share of the Title Insurers with the top 4 companies controlling 82% market share (a dynamic that supports the industry’s pricing power).

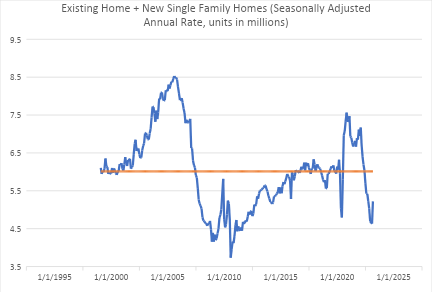

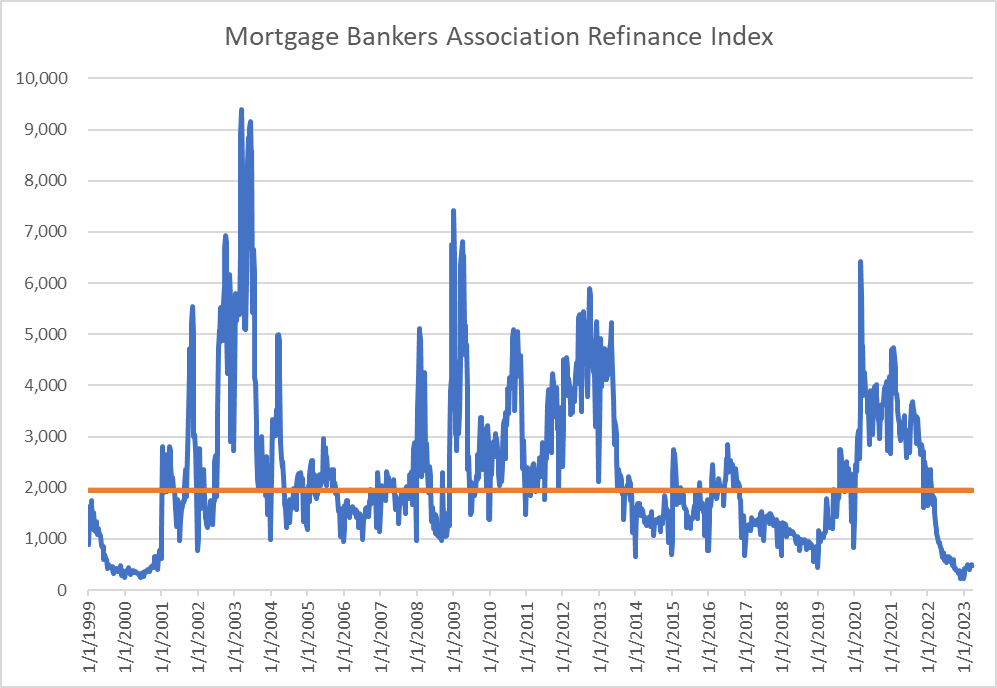

The charts below show the currently depressed levels of home purchase and mortgage refinance activity due to the surge in interest rates. The first chart below shows that in the fourth quarter of 2022, purchase activity collapsed to levels not seen since the Great Financial Crisis and the peak lock-down period during COVID. The second chart shows that mortgage refinance activity is at the lowest level in the last three decades.

As activity levels recover from the currently depressed levels (purchase +30% upside and refinance +300% upside from the trough in fourth quarter 2022) I estimate FNF, FAF, and STC are trading at normalized earnings yields of 30% (FNF), 15% (FAF), 20% (STC), respectively. At these levels of earnings power, I see potential stock returns of 2-3x current share prices. Given the entrenched nature of this oligopoly, their strong balance sheets, and attractive 4-5% dividend yields, I am happy our Partnership gets paid to wait for activity levels to normalize (per the charts above, activity can snap back very quickly!).

It was a busy first quarter and I am excited about our new portfolio allocations as well as the current pipeline of new ideas (more to come in the next quarterly letter). We’ve significantly diversified the industries represented in the portfolio while investing in high quality businesses possessing strong return profiles. My family balance sheet remains fully invested in our partnership and I am excited about our future. Thank you for your trust and please feel free to reach out anytime.

Your partner and fiduciary,

Faris Jafar, Chief Executive Officer

Phone: (734) 678-8562