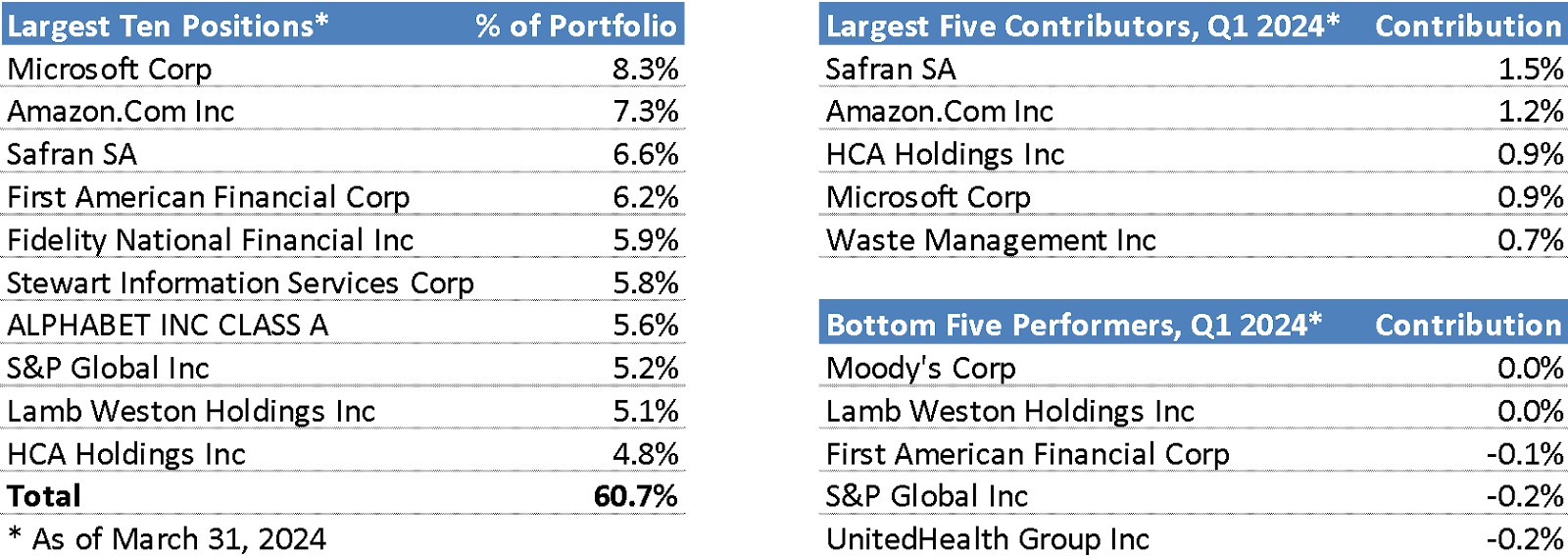

Equity markets were buoyed by positive employment and economic data which generally benefited stocks that skew to procyclical sectors. Bond markets (and less cyclical equities) lagged as the stronger economic data, elevated federal government deficit spending, and higher oil prices fueled concerns around prolonged inflation. Given this macroeconomic backdrop, I am pleased to report that our top performing investments were balanced across a diverse group of sectors including Aerospace, Consumer Discretionary, Health Care, Technology, and Waste Collection while our stocks in Credit Rating Agencies and Title Insurance underperformed (despite solid business results) due to higher interest rates. I am encouraged by the strong operating earnings of our companies, the broad-based sector contributions to Fund returns, and the attractive valuation of our portfolio.

Portfolio Update

In early March I exited our investment in Intuit as the shares became too expensive to fit our future return criteria. I allocated the proceeds to sectors and select stocks that are significantly dislocated for transitory reasons, as follows:

- Credit Ratings Agencies: the recent spike in interest rates has pressured shares despite solid operating earnings and business momentum. I believe this investment can double over the next five years as interest rates normalize

- Title Insurance: higher interest rates and regulatory noise have the sector trading for an ~20% earnings yield and one of the biggest discounts to the market in recent history. Frivolous regulatory headlines are common in this industry and I believe the current narratives will prove similar. I expect the inflecting recovery in housing activity will lead to multiples-of-money on our investment

- UnitedHealth Group: a cyber-attack and a DOJ antitrust investigation have pressured shares of this great franchise to a 7% earnings yield (one of the cheapest prices for the shares in the last decade). While these headlines make for splashy news, I expect very minimal impact to the franchise and our investment has the potential to double from current levels over the next five years

- Lamb Weston Holdings: larger-than-expected operating disruptions due to an ERP transition (software system upgrade during Q3 2024) drove shares to the lowest valuation in the company’s history (10% earnings yield). The company has reported that the transition disruption is over and I expect several multiples-of-money on our investment as the company accelerates share repurchases and earnings continue to grow

On a consolidated basis, our growing companies are valued at an attractive 5% earnings yield and portfolio beta of 0.88. Considering these factors combined with the strong business characteristics of our diverse, dominant, and resilient franchises, I believe the expected return profile of our partnership is very bright. My family balance sheet remains fully invested with you and I am excited about our future. Thank you for your trust and please feel free to reach out anytime.

Your partner and fiduciary,

Faris Jafar, Chief Executive Officer

Phone: (734) 678-8562