The reasons for downward pressure on global asset values this year remain the same (i.e. inflation, interest rates, recession and the Ukraine/Russia conflict). As long-term investors, our strategy prefers dominant businesses that can scale globally (to capture larger market opportunities than any single country can offer) and have a long runway for structural growth above GDP. The Federal Reserve’s decision to accelerate interest rate hikes created incremental short-term headwinds on assets with the aforementioned attributes – specifically, the nearly +20% appreciation of the U.S. dollar reduces the value of revenues generated outside of the United States and higher interest rates have an outsized impact on long-duration assets (i.e. higher growth businesses that are expected to generate a larger proportion of cash flows in the future versus businesses with slower cash flow growth). Regardless of these short-term dynamics, we remain focused on the long-term and our strategy is unchanged. We own dominant, growing franchises, with substantial cash flow and healthy balance sheets. Our portfolio companies have demonstrated an ability to do well in a variety of economic environments and I am confident in their ability to navigate the current cycle and emerge even stronger as weaker competitors struggle during macroeconomic duress.

As Morgan Stanley recently observed in its October 4th, 2022 research report titled “Where Are We Trading Now: Where are Multiples as 4Q Trading Begins” – the Internet sector’s valuation is “25%/16% below the five/ten year average while mega caps Amazon and Google are trading at/below long-term trough multiples”. To be clear, this dynamic is not isolated to the Internet sector and is observed throughout our portfolio. It is my view that trophy assets do not stay at bargain prices for very long, and the following data helps contextualize the extreme volatility we have already endured and why I am excited about our path forward.

Exhibit 1: U.S. Government 2 Year Treasury Note Yield

- The recent rise in interest rates (~0.2% to ~4.25% in just one year) represents the sharpest increase in 20 years

- While it generally takes several months for higher interest rates to impact the broader economy and inflation, stocks and bonds have been quick to respond to the interest rate volatility

- There is already evidence that the deflationary effects of higher interest rates are extending beyond the financial markets and into the real economy (more on that below)

- Observing the chart below, interest rates oscillate over time and one must be careful not to extrapolate extreme moves into perpetuity

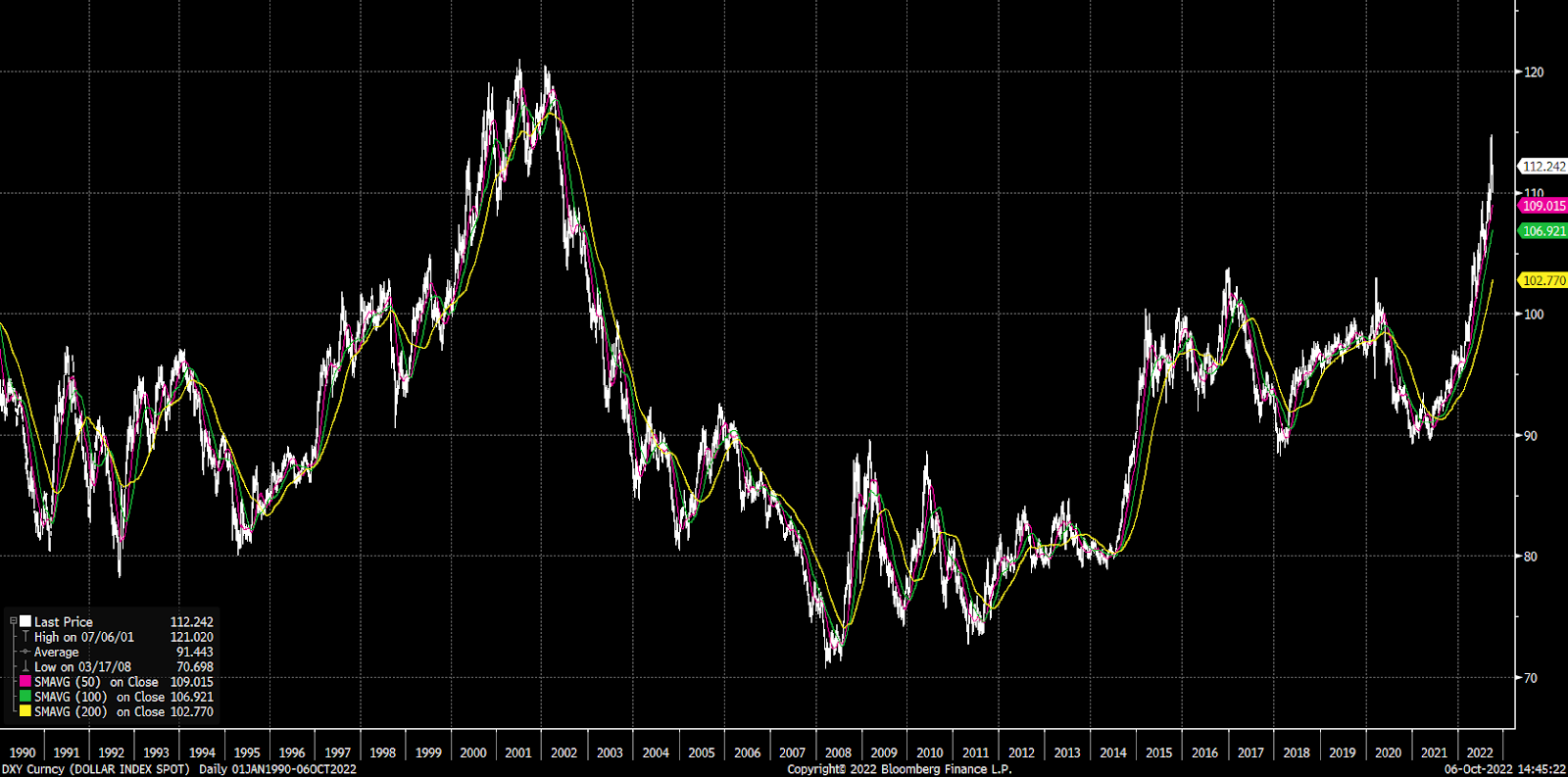

Exhibit 2: U.S. Dollar Index

- The sharp rise of the U.S. dollar relative to foreign currencies represents a headwind to companies that generate revenue outside of the United States (since foreign currencies become relatively less valuable in dollar terms)

- Much like the observation made above, the relative dollar value oscillates over time so one must be careful not to extrapolate the extreme moves into perpetuity

- It’s worth noting that companies with pricing power may elect to increase prices to offset this headwind (e.g. Apple has recently announced price increases in select international markets for this reason)

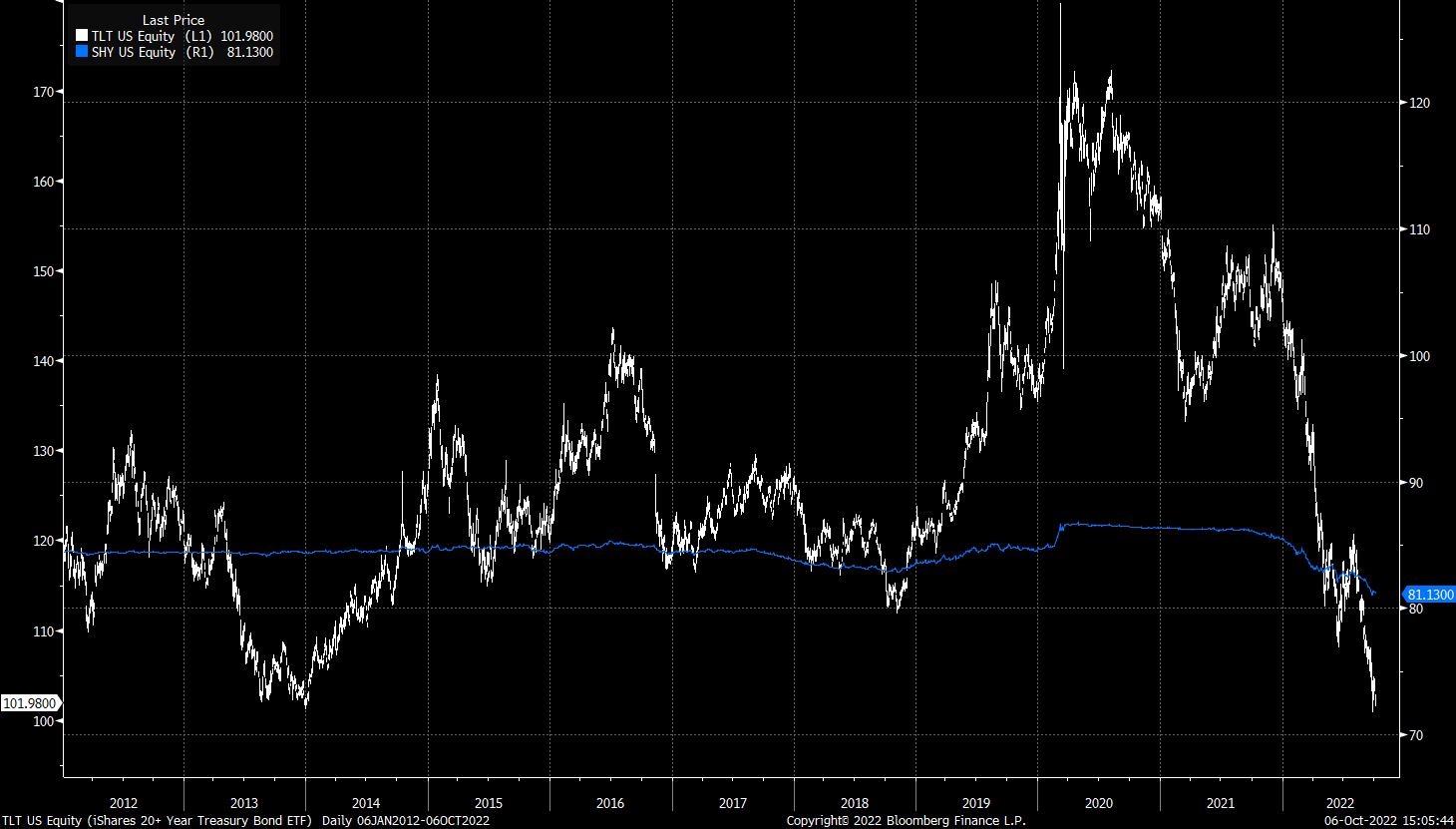

Exhibit 3: Long Duration versus Short Duration Performance

- The white line represents an index of U.S. Federal Government Treasury bonds that mature in 20 years or more (Long duration)

- The blue line represents an index of U.S. Federal Government Treasury bonds that mature in 1-3 years

- While the relationship fluctuates over time, the Long duration bonds are down -31% this year (marking the lowest level in 10 years) while the shorter duration bonds are only down -5%

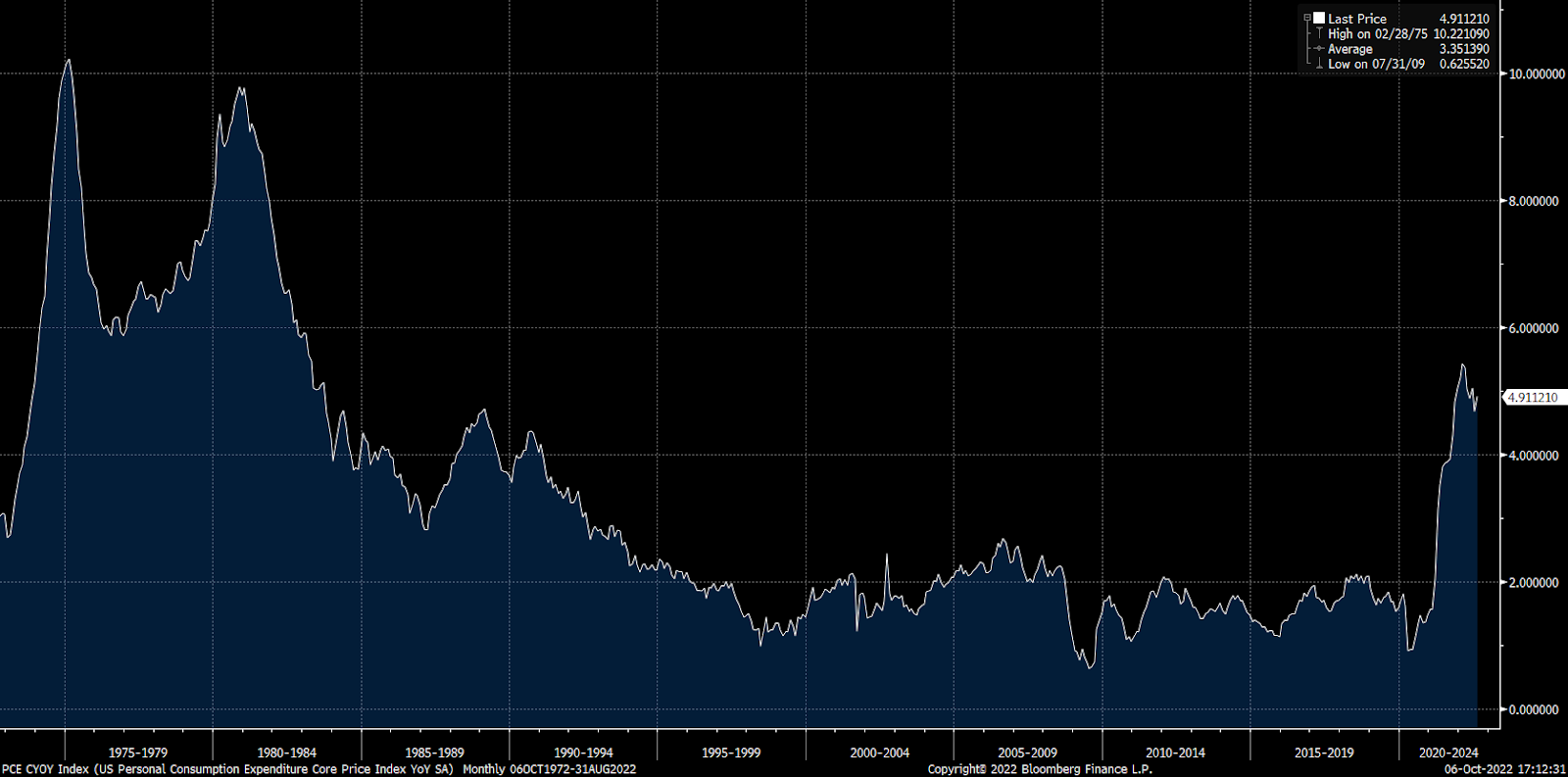

Exhibit 4: Inflation and the Stock Market (S&P 500)

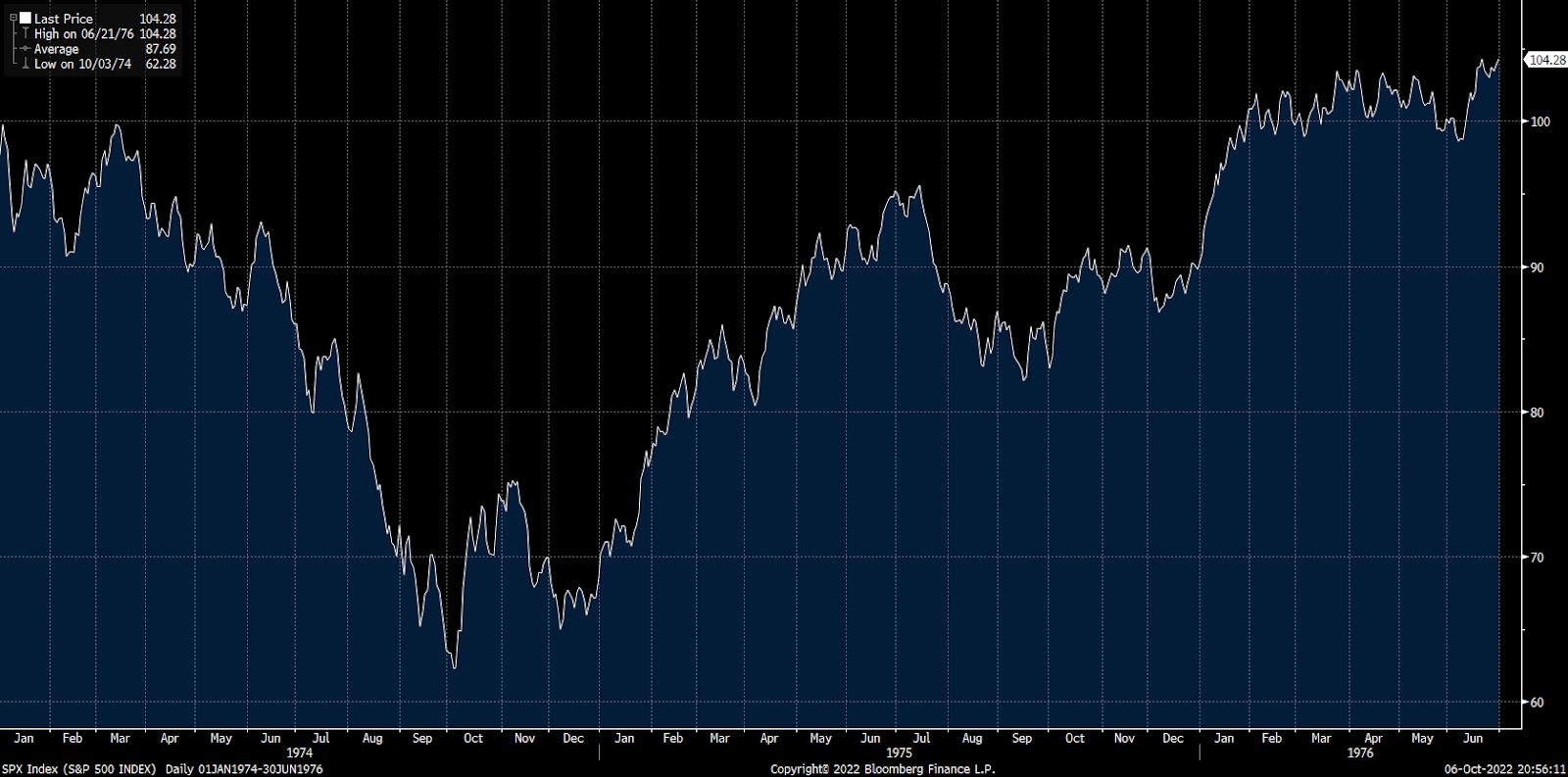

- Chart 1 illustrates that inflation has been with us for decades with the most glaring surges occurring in the 1970s/1980s, and now most recently in the post-Covid recovery

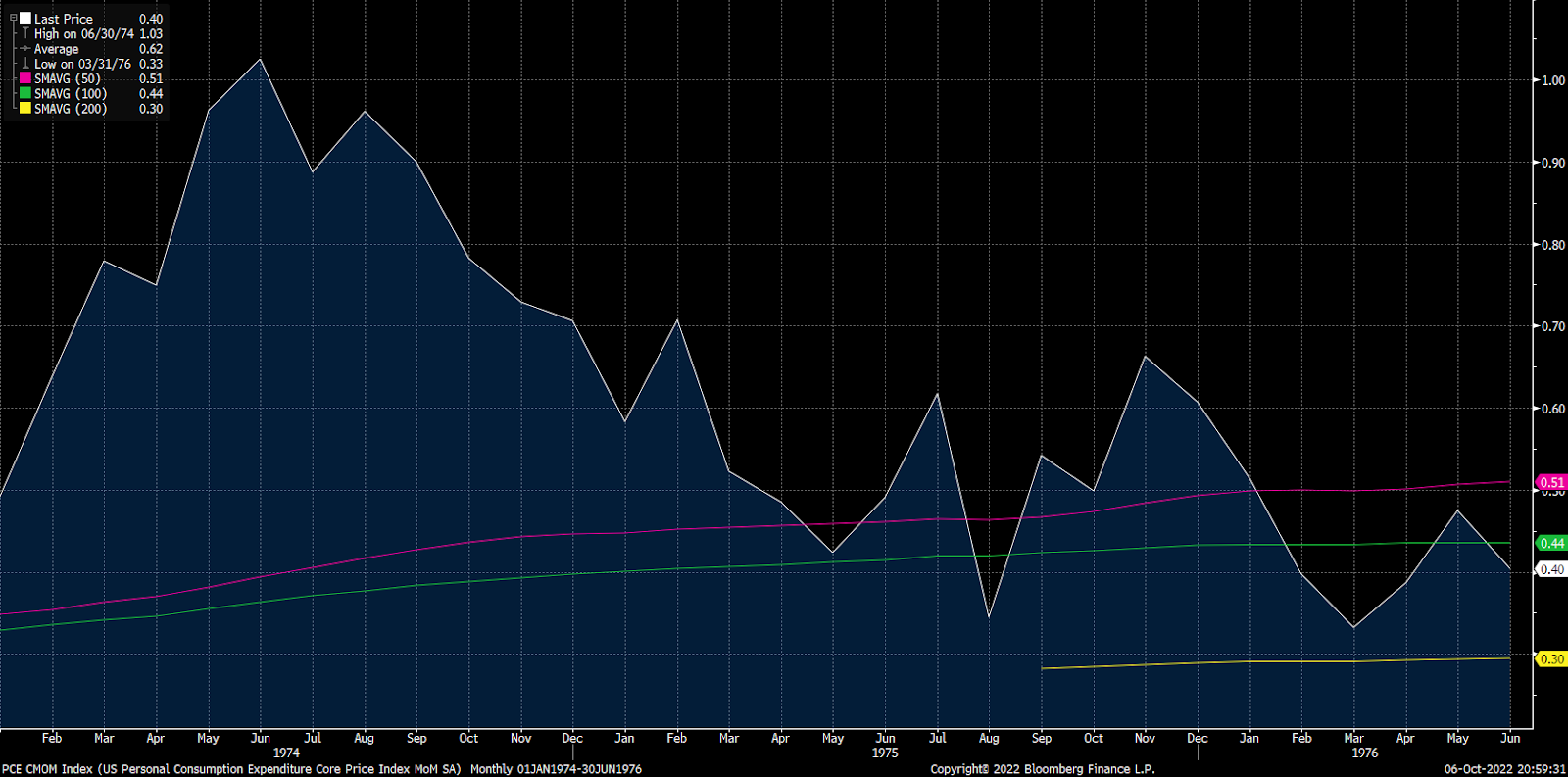

- During the inflation spike in the 1970s, year-over-year core inflation peaked in February of 1975, however, the stock market actually bottomed five months earlier in October of 1974 as the month-on-month readings began to show sequential deceleration in inflation (see Chart 2)

- Chart 3: By 1975 (just 9 months from the October 1974 bottom), the market recovered the losses experienced in 1974 and went on to make new highs in 1976

Chart 1: Core Personal Consumption Expenditure Index Year-over-year Inflation (“Core PCE”)

Chart 2: Core PCE Inflation Month-over-Month (January 1974 – June 1976)

Chart 3: S&P 500 Stock Index (January 1974 – June 1976)

Exhibit 5: The Path Forward

- There are several signs that the Federal Reserve’s actions are already taking effect, and given the lag time before policy impacts the economy (first hikes were in March 2022), there’s potential for the deflationary effects to become more noticeable in the near future. Selected examples include:

- The “Wealth Effect”: As I mentioned earlier, financial assets have responded quickly and are down sharply year-to-date:

- S&P 500 -25%; Nasdaq -32%; Russell 2000 -26%; LQD (Investment Grade Bond Index) -23%

- Commodities that serve as leading indicators are down year-to-date

- Copper -23%; Steel -43%; Lumber -63%

- Used Car prices are down -13% year-to-date

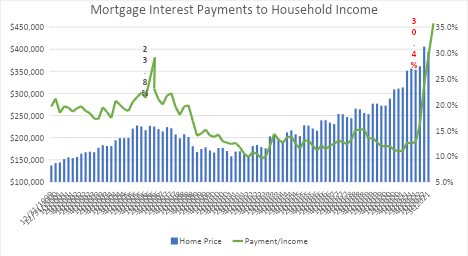

- 30-year mortgage rates have gone from 3% to 7% making a home purchase the most expensive in 20 years. The historically poor affordability is resulting in a buyer’s strike as demonstrated by Existing Home sales down -21% year-to-date

- While home prices have shown recent signs of cooling, the chart below shows there is good reason to believe that there will be significant pressure in home prices to get affordability back in line with sustainable levels

- Recent rental market data aggregators have cited sequential declines in rents

- The “Wealth Effect”: As I mentioned earlier, financial assets have responded quickly and are down sharply year-to-date:

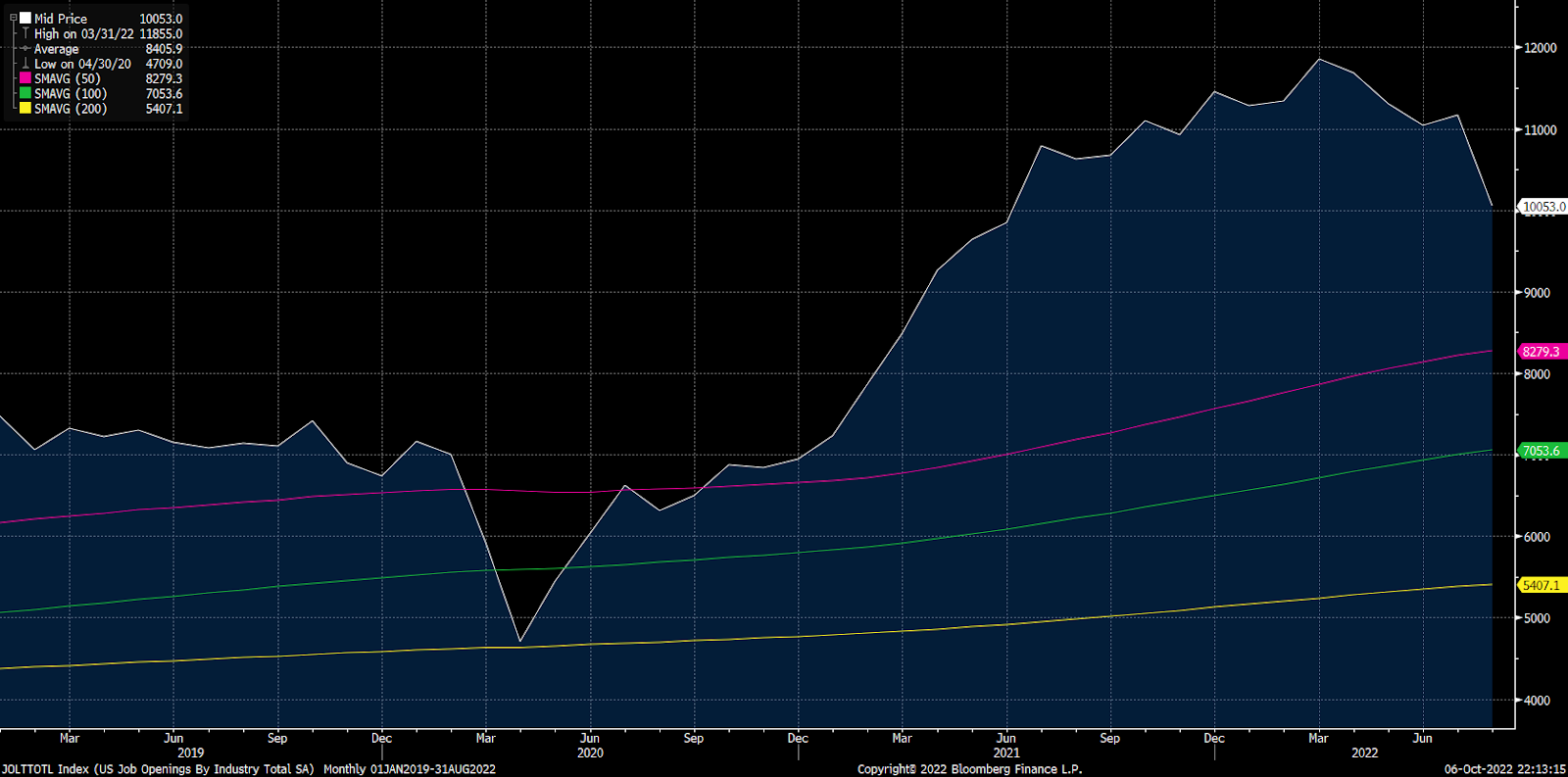

- Wage growth has moderated as job openings (demand) are falling which will bring better balance in the workforce

- The chart below shows U.S. job openings recorded by the Bureau of Labor Statistics. The August reading showed a decline of -1.8mm job openings from the March peak of 11.9mm job openings

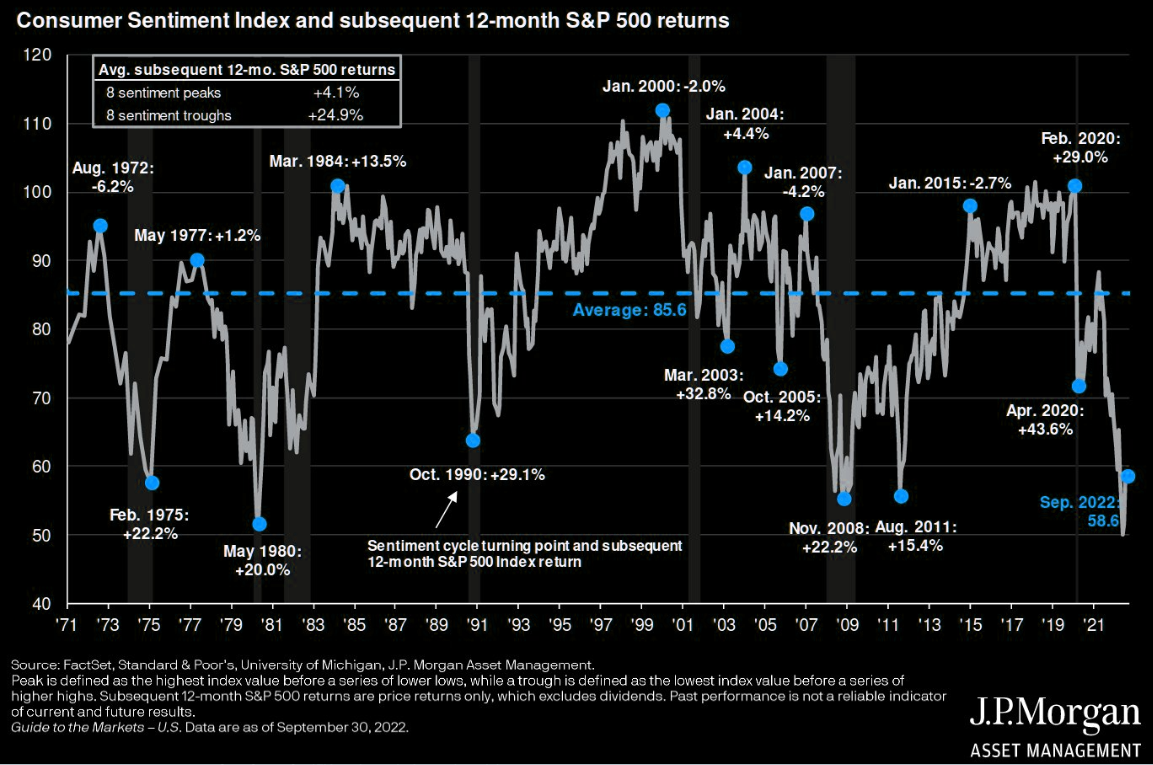

- University of Michigan Consumer Sentiment Index is at historical lows. Per the chart below (credit to J.P. Morgan), Consumer Sentiment lows are generally followed by positive market performance

- Similarly, investor sentiment is now at levels seen in April 2009 (see chart below, credit to Morgan Stanley)

In 2008 during the Great Financial Crisis, Warren Buffett wrote an Op-Ed in the New York Times titled “Buy American. I Am.” (please let me know if you would like a full copy of the article). The message from the legendary long-term investor is powerful particularly with respect to the impact of psychology on investing. Below is an excerpt:

“THE financial world is a mess, both in the United States and abroad. Its problems,

moreover, have been leaking into the general economy, and the leaks are now turning

into a gusher. In the near term, unemployment will rise, business activity will falter and

headlines will continue to be scary.

So … I’ve been buying American stocks. This is my personal account I’m talking about,

in which I previously owned nothing but United States government bonds. (This

description leaves aside my Berkshire Hathaway holdings, which are all committed to

philanthropy.) If prices keep looking attractive, my non-Berkshire net worth will soon be

100 percent in United States equities.

Why?

A simple rule dictates my buying: Be fearful when others are greedy, and be greedy when

others are fearful. And most certainly, fear is now widespread, gripping even seasoned

investors. To be sure, investors are right to be wary of highly leveraged entities or

businesses in weak competitive positions. But fears regarding the long-term prosperity of

the nation’s many sound companies make no sense. These businesses will indeed suffer

earnings hiccups, as they always have. But most major companies will be setting new

profit records 5, 10 and 20 years from now.

Let me be clear on one point: I can’t predict the short-term movements of the stock

market. I haven’t the faintest idea as to whether stocks will be higher or lower a month —

or a year — from now. What is likely, however, is that the market will move higher,

perhaps substantially so, well before either sentiment or the economy turns up. So if you

wait for the robins, spring will be over.”

I generally try to keep the focus of my letters on the fundamentals of our businesses because I believe that the quality and trajectory of a business is what ultimately dictates long-term investment returns (it’s worth mentioning that our companies have reported very impressive results and encouraging outlooks for their businesses). That said, given the magnitude of the recent market turmoil I thought it might be helpful to provide context on the various dynamics at play, their progression to-date, and share how I am thinking about the future. In short, I expect many of the headwinds we have faced to subside (as shown above, many data points suggest we are closer to the end of this interest rate/inflation driven correction than the beginning), and I expect our portfolio of dominant, structurally growing, cash-rich businesses to set new profit records in the years ahead. As always, my personal family balance sheet is fully invested in our Partnership and am excited about our long-term profit potential. Thank you for your trust and please feel free to reach out anytime.

Your partner and fiduciary,

Faris Jafar, Chief Executive Officer

Phone: (734) 678-8562