Market sentiment softened late in the quarter due to three factors contributing to economic recession concerns, all of which are transitory in my view:

- Sharp increase in U.S. Treasury bond interest rates

- Higher oil prices due to Saudi Arabia and Russia announcing oil production cuts

- Resumption of student loan payments which had been on hold since the onset of the pandemic in 2020

While the Federal Reserve has paused raising interest rates, U.S. Treasury bonds (and the broader bond market) have come under significant selling pressure due to an enormous budget deficit which now amounts to approximately 7-8% of U.S. GDP (double pre-pandemic deficit levels). In other words, the U.S. government is taking on $1.5 trillion of incremental debt this year because it is spending more than it receives in tax revenue – a dynamic that is expected for several years. Politics aside, I believe the market impact of this issue is transitory because the trajectory of inflation is what will ultimately dictate investors’ willingness to buy bonds and longer duration assets such as equities – and inflation continues to show signs of cooling.

Regarding oil prices, commodity prices can be volatile in the short-term (oil reached $130/barrel last year and now trades $87/barrel), but any sustained period of elevated prices generally creates some demand destruction and brings on new supply, which ultimately leads to lower prices. The recent human tragedy in the Middle East could create additional oil price volatility, however, it appears that diplomatic efforts are in place to avoid the conflict from spreading to surrounding countries. Regardless, I do not expect a material impact to our portfolio of businesses from oil price volatility.

The resumption of student loan repayments will eat into consumer discretionary spend, however, this is a short-term impact to demand and will also have the added benefit of cooling inflation. It is worth noting that incomes are ~13% higher than pre-pandemic levels and the job market remains healthy with a low unemployment rate and an increasing participation rate (approaching pre-pandemic levels). In other words, demand for workers remains healthy, and workers who left the work force during the pandemic are now returning to the labor pool which creates a more balanced labor market, softens upward wage pressure, and helps cool inflation.

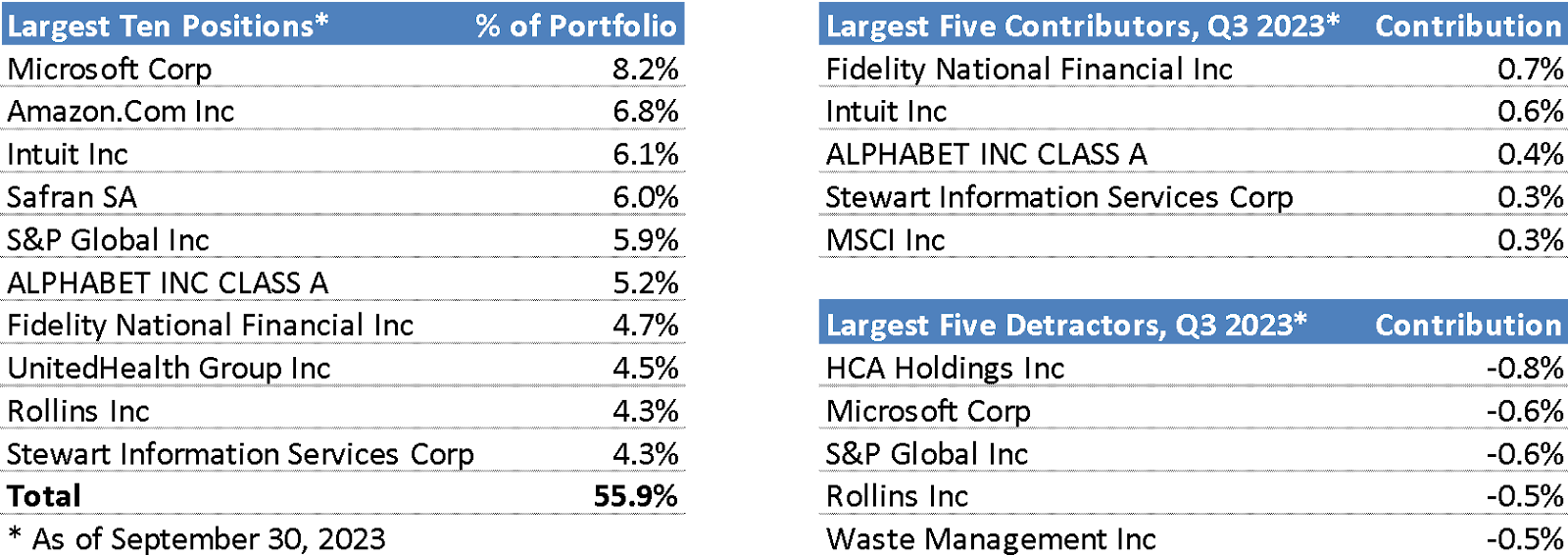

Portfolio Update

In July, I sold the Fund’s investments in Apple and MSCI due to their share prices becoming too expensive relative to their earnings growth potential. Both companies are excellent franchises and I would be happy to buy them back at more attractive prices, in the interim I will recycle the capital into new and existing investments that offer much better return profiles. For context, our portfolio currently trades at a 5.25% earnings yield (based on Wall Street estimates), which in many cases represents near trough valuations for our companies and unusual discounts relative to the broader market. I also believe Wall Street estimates are too low for many of our companies, which combined with the trough valuations makes for compelling buying opportunities.

Regarding new ideas, there has been significant dislocation to stock prices in the healthcare and food sectors due to the potential disruption from weight-loss drug innovation (“GLP-1”). It is rare for many of the companies in these sectors, which are generally considered durable and economically resilient, to see such discounted stock prices and I look forward to sharing my research findings (and new investments) in the next investor update.

As always, my family balance sheet remains fully invested in our partnership and I am excited about our future. Thank you for your trust and please feel free to reach out anytime.

Your partner and fiduciary,

Faris Jafar, Chief Executive Officer

Phone: (734) 678-8562