Portfolio performance was driven by inflections in strategic allocations to sectors that I expect will generate multiples-of-money for our Partnership. In September, the Federal Reserve started reducing interest rates as its focus shifts away from stemming inflation to protecting the labor market and supporting economic activity. Historically, the labor market gets worse (i.e. unemployment deteriorates) for a few quarters after the commencement rate cutting. While it is possible that the Federal Reserve is late in beginning the rate cuts, the most important thing to remember is that the Federal Reserve intentionally caused the economic deceleration (which has weighed on the private sector for over two years) and the Federal Reserve is now in the process of accelerating the private sector (and has ample capacity to do more if need be) – Fed Chair Jerome Powell has made this last point explicitly clear in recent communications. I believe we are well positioned for strong investment returns given our strategic allocations to durable franchises that will accelerate in this environment and a high-quality portfolio trading at a discount to a frothy market.

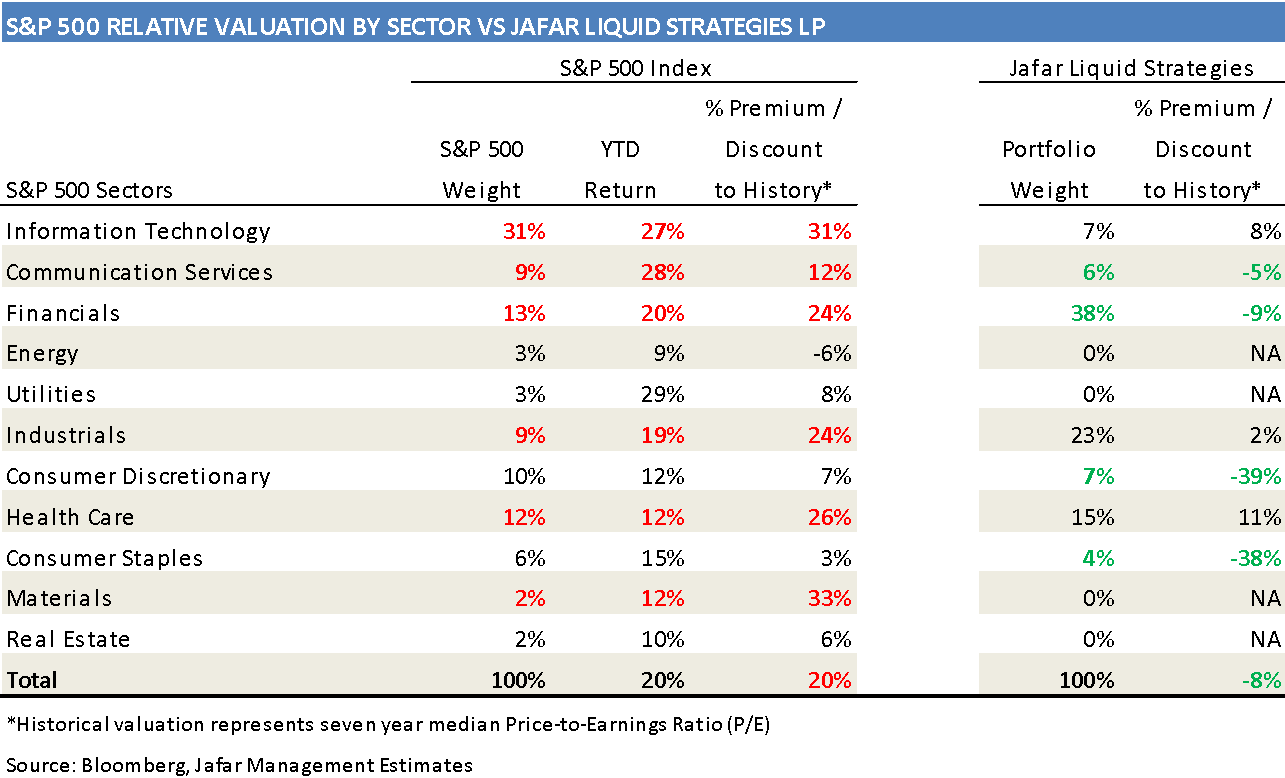

The table below illustrates the froth in the market juxtaposed to the significant discount embedded in our portfolio. The S&P 500 trades at a +20% premium to its historical valuation whereas our portfolio trades at an 8% discount to our assets’ historical valuations. Furthermore, our investments’ relative valuations are more attractive across every sector represented in our portfolio relative to the S&P 500. This dynamic is due to the following active portfolio management activities that aim to optimize returns while maintaining a defensive posture:

- Reducing exposure to investments that become too expensive and therefore offer less attractive future returns

- Avoiding the frothy pockets of the market that have dubious sustainability and hype-driven returns (e.g. Artificial Intelligence, China stimulus, etc). Per the table below, the volatile portions of the Information Technology, Financials, Materials, Industrials, and Healthcare sectors trade for +24-33% premia relative to their history

- Take advantage of market dislocations by allocating capital to high-quality franchises trading near trough valuations with the opportunity to make multiples-of-money on our investment

- Maintain a liquid, diversified portfolio across multiple industries and number of investments

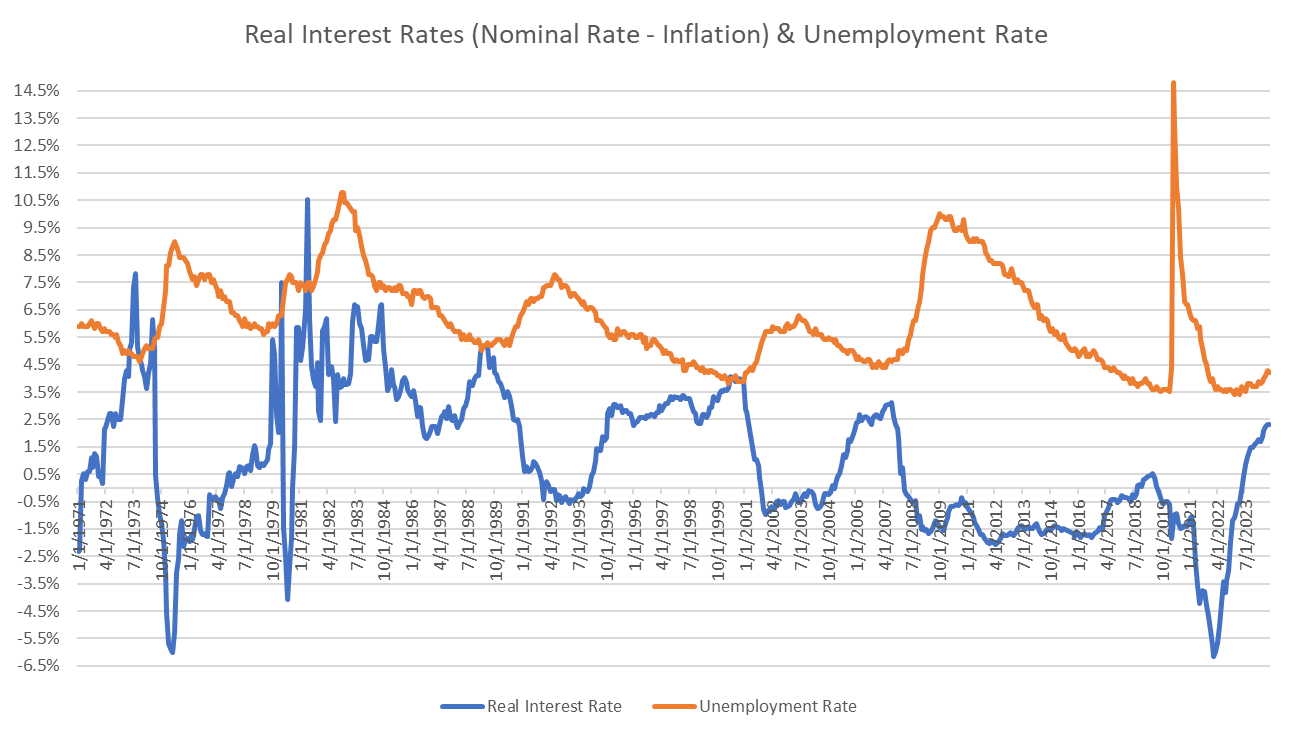

The chart below shows why the Federal Reserve is now focused on protecting the labor market. Since the 1970s, in every instance where real interest rates become too restrictive and peak (“real interest rate” defined as Federal Funds Rate minus Inflation), unemployment increases for the subsequent 6-12 months. Unlike in prior cycles, this time unemployment has been increasing before the Federal Reserve started cutting rates, which is why one could argue the Federal Reserve is late. Regardless, given real rates remain elevated, the Federal Reserve has ample capacity to accelerate its efforts if needed to protect the labor market. With the labor market likely deteriorating and the broader equity market at historically extreme valuations driven by volatile sectors, I believe our portfolio is advantaged given the significant relative discount and strategic allocation to market leading franchises in sectors that will accelerate as we progress through this part of the cycle.

Portfolio Update

There were no new positions added nor exits during the quarter but portfolio management remained quite active. I took advantage of several dislocations to add to positions that reached trough valuations, namely: Alphabet, Visa, and Waste Management. All of which are very high-quality franchises that I believe will generate 2-3x our investment over the next five years. Lastly, I finalized our tax-loss harvesting activities which largely offset most of our realized gains this year.

A couple of items worth mentioning:

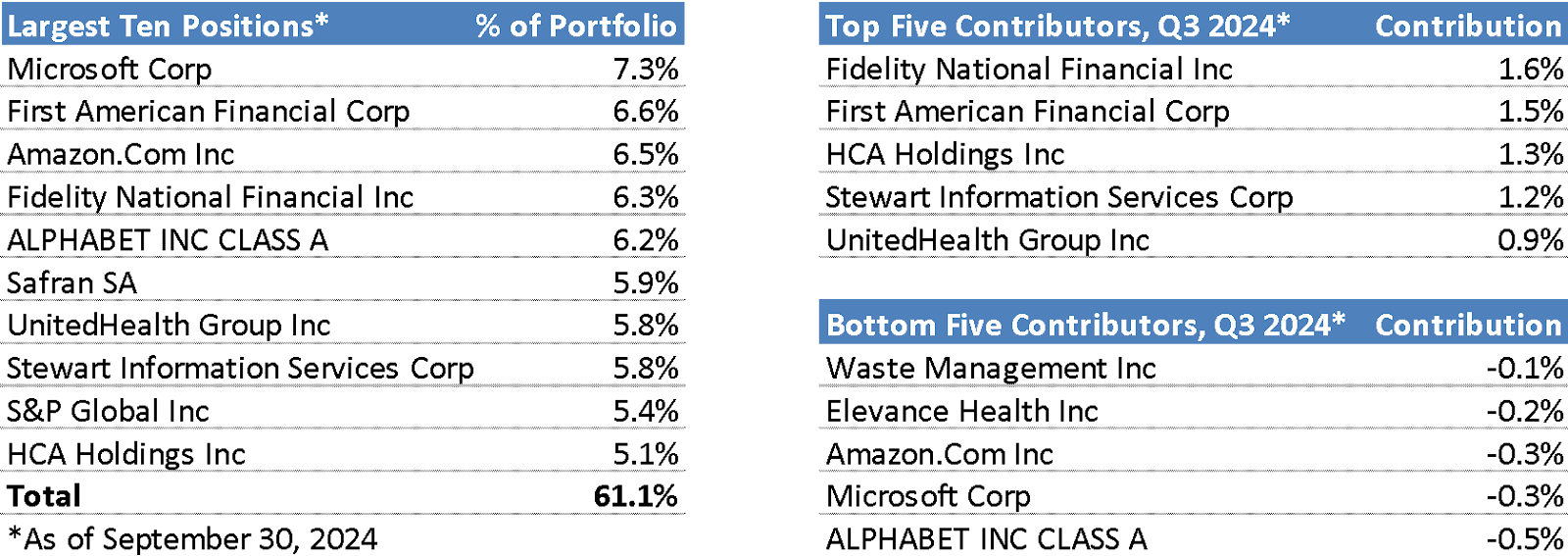

- While our Top Five Contributors for the quarter included all our Title Insurance investments, our collective investments in the Financial Services sector (which includes the Ratings Agencies S&P Global and Moody’s) were by far the largest contributors to our Partnership’s profits this quarter. This is an example of the type of strategic allocations I have made to invest in high-quality oligopolies that will accelerate during this part of the economic cycle due to their businesses having been artificially depressed in the high-interest rate environment. While these investments have performed nicely, I believe it is still early days and I expect them to generate 2-3x returns over the next five years.

- I believe our allocation to dominant “old economy” businesses that can leverage Artificial Intelligence technology is one of our strongest strategic pillars for driving significant future investment returns. A recent presentation from Thomas Kurian, the CEO of Google Cloud, at the Goldman Sachs Communacopia + Technology conference provided some exciting real-time insight into this theme:

- “Hiscox, one of the largest syndicates in Lloyd’s of London [an insurance company], introduced the first AI-enhanced lead underwriting model. So when they insure property risk, it used to take them months to calculate the entire portfolio. A single property took three days. It takes a few seconds now. What used to take months now takes a matter of days.”

- “If you call Verizon, you’re talking to our chat system and our call system. 60% containment rate [problem solved without talking to a human agent], high rate of call deflection.”

- “If you’re driving a General Motors vehicle and you hit OnStar, you’re talking to our conversational AI system”

- “[in hospitals] we work with nursing staff, for example, to do live handoffs of patients. It saves about 6 hours in a 24-hour day. And one of the leading hospitals is talking at a conference today that they estimate when rolled out it’ll save them $250 million.”

- “We’re working with the largest health insurance company in Germany. They have a huge amount of claims coming in. On average a claim, they need to read 800 policy documents to determine if a claim is valid or not. They use our technology. It helps take 23 to 30 minutes down to 3 seconds.”

- Lamb Weston: high interest rates and inflation have led to a weak consumer spending environment particularly in the restaurant industry. After nearly a year of negative foot-traffic to restaurants (a historically abnormal duration of softness), the restaurant industry is taking aggressive action to reduce menu prices and stimulate demand. In the most recent quarter, Lamb Weston reported a meaningful improvement in sales volume reflecting the recent stabilization in restaurant demand and embarked upon a substantial cost-savings initiative to enhance profitability. I believe this inflection in revenue and profitability, as well as better balance in the supply/demand dynamics for French fries will drive robust profit acceleration leading to a 2-3x return on our investment over the next 5 years.

While the media will be distracted by the upcoming U.S. elections, it is my belief there is likely little market or economic impact from the result. In my view, the single most important driver of the economy will be the pace of interest rates cuts and the stability of the labor market. I believe the significant discount embedded in our portfolio, limited exposure to the frothiest pockets of the market, and differentiated strategy to the A.I. theme positions us well for very attractive investment returns. My family balance sheet remains fully invested and I am grateful to be in your service. Thank you for your trust and please feel free to reach out anytime.

Your partner and fiduciary,

Faris Jafar, Chief Executive Officer

Phone: (734) 678-8562