While the volatility in 2022 was disappointing, there is reason for optimism as many of these headwinds are improving. Specifically:

- The U.S. dollar has depreciated over 10% from the September peak which, at current levels, would result in a tailwind to our portfolio companies’ revenue in 2023

- Inflation is cooling and the Federal Reserve has signaled the interest rate hiking cycle is nearing an end

- After rising from 1.5% to a peak of 4.25% in September, 10-year treasury yields have declined to 3.5% which should support longer duration assets

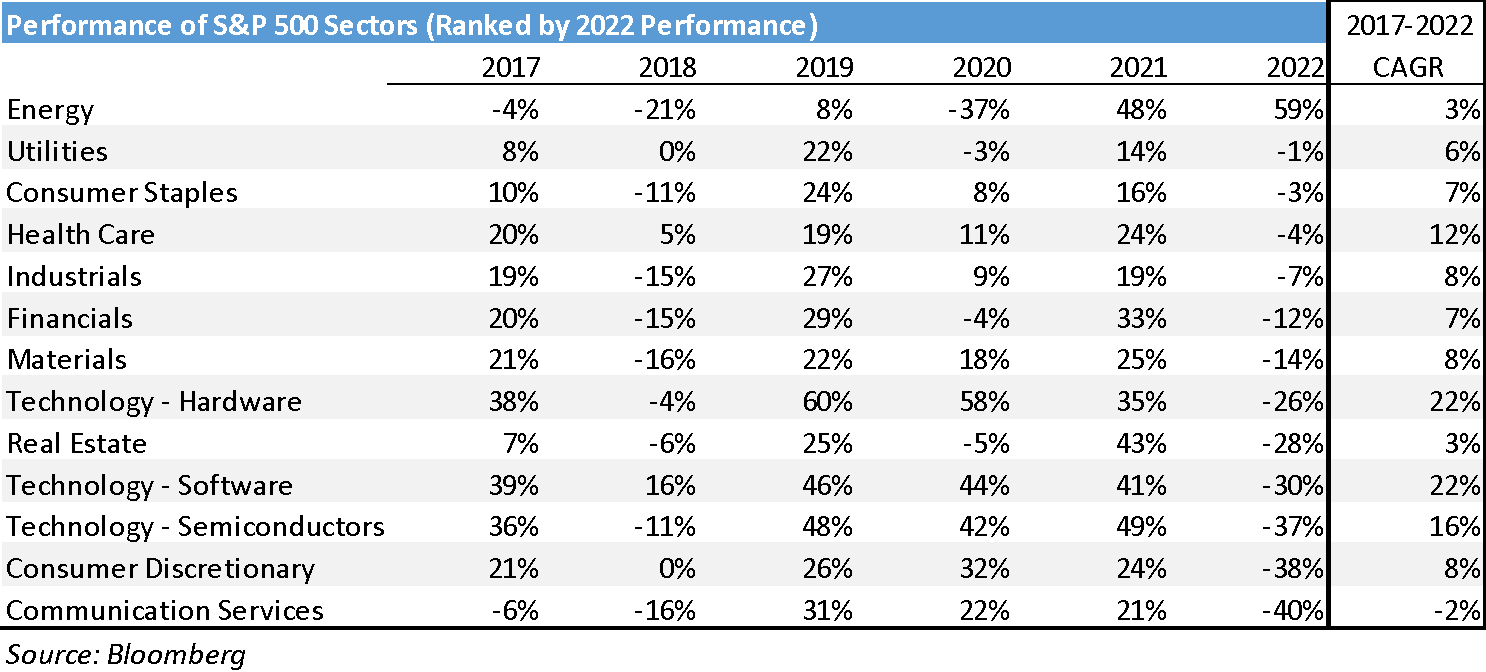

A long-term oriented strategy will inevitably face periods of underperformance given the volatility inherent in short-term market conditions. That said, underperforming is never welcome nor was the performance of 2022 one that I’d ever like to experience again (more on this later). The chart below shows how extreme the dispersion across subsectors was in 2022. In short, the Energy index was a tremendous outlier at +59% bringing it’s compounded annual performance since 2017 to +3% while the best performing sectors since 2017 were the most significant underperformers. For reference, our largest allocations are categorized in Technology – Software (e.g. Microsoft which was down -29%), eCommerce (e.g. Amazon which was down -50%) as subcategory of Consumer Discretionary, and Internet Advertising (e.g. Alphabet which was down -39%) as a subcategory of Communication Services.

As fundamental investors, I believe it is important to maintain intellectual honesty and humility so that we can make the best capital allocation decisions. With that in mind, the following are my primary reflections on 2022 and the corresponding takeaways for the future:

- We remain committed to our long-term investment framework. Nothing about our 2022 experience changes our investment approach or the type of businesses we wish to own. Over the long-run, it is my belief that the durability and trajectory of a company’s cash flows are what ultimately drive investment returns. We will continue to invest in businesses that we believe are structurally advantaged, market leading franchises with attractive growth prospects.

- While the growth rates of eCommerce and Software companies certainly decelerated after the pandemic surge and during the recent weakening macroeconomic environment, one of the most important factors to consider in our benchmarking of “structural winners” is that they maintained those extraordinary gains and continue to grow their share of the global economy

- Absent an outright exit of our strategy, the table above shows that 2022 was going to be a difficult year for our largest portfolio allocations. I view the attractive high-quality characteristics of our portfolio companies (structural growth, recurring revenue, strong cash generation and healthy balance sheets) as a first line of defense to help weather market volatility, however, the anomaly of the pandemic, the subsequent government responses (including monetary and fiscal actions), geopolitical instability and the aforementioned technical headwinds resulted in substantially more volatility than I expected.

- Regardless of whether I agree or disagree with the volatility, I am mindful of the fact that if it can happen once (anomaly or not), that is sufficient evidence that it can happen again. In addition to maintaining a conservative balance sheet and diversified portfolio, we have other tools at our disposal that I believe can help navigate future volatility. Examples include:

- Tactically reducing position sizes as future return expectations become less attractive relative to other opportunities

- Further diversify the industries represented within the portfolio

- Allocations to cash and other liquid interest-bearing securities when waiting for more attractive entry points for equities

- Regardless of whether I agree or disagree with the volatility, I am mindful of the fact that if it can happen once (anomaly or not), that is sufficient evidence that it can happen again. In addition to maintaining a conservative balance sheet and diversified portfolio, we have other tools at our disposal that I believe can help navigate future volatility. Examples include:

Looking into 2023, we are now at the point where the negative impacts of higher interest rates will become more apparent to the broader economy – indeed, several macroeconomic indicators are now signaling a slowdown. The good news is that the technical headwinds facing our portfolio are easing and many of our portfolio companies are trading at historically low valuations – suggesting that macroeconomic deterioration has been factored into the stock prices. In the event of macroeconomic softness, I expect our portfolio companies to take share from weaker competitors and emerge even larger as the economy accelerates. Either way, we own a portfolio of dominant, highly profitable, structurally growing franchises and our focus remains on the fundamental drivers that I believe will ultimately drive investment returns. My family balance sheet remains fully invested in our partnership and I am excited about our future. Thank you for your trust and please feel free to reach out anytime.

Your partner and fiduciary,

Faris Jafar, Chief Executive Officer

Phone: (734) 678-8562