Cooling inflation, lower interest rates, and stable economic data led to an improvement in market sentiment which drove broad-based positive Fund performance in the quarter. I believe our diversified portfolio of market-leading franchises is well positioned for continued momentum given a significant portion of our investments are still undervalued and poised for strong earnings growth. As testament to my conviction in our Partnership’s profit potential, I invested 100% of my 2023 fees into the Fund (as I have done every year since inception).

Portfolio Review

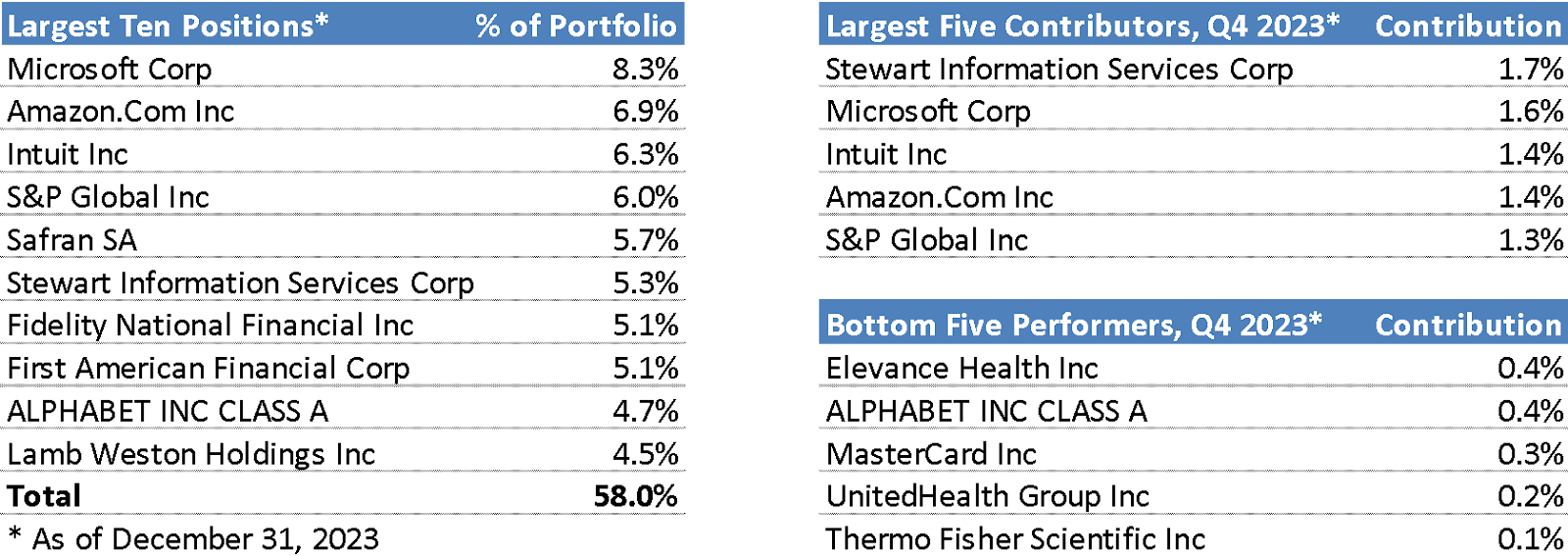

Throughout the year I reduced positions that became too expensive and reallocated to other opportunities that presented significantly better value (i.e. better investment return potential). I believe this active recycling of capital, combined with the very strong earnings trajectory within the existing portfolio sets a strong foundation as we progress into 2024 and beyond. To quantify the impact of these dynamics, our current portfolio trades for a ~5% earnings yield and ~2/3 of the portfolio trades near trough valuation levels. This active management approach enabled our Partnership to significantly grow the dividend yield from nearly zero a few years ago to approaching 2% today. The strategic benefits to our Partnership are two-fold: first, by recycling expensive investments for alternatives that offer better value, we amplify the partnership’s future return profile while growing the dividend yield more than the companies themselves are growing organically. Second, we can use the cash from dividends to redeploy capital opportunistically and compound returns.

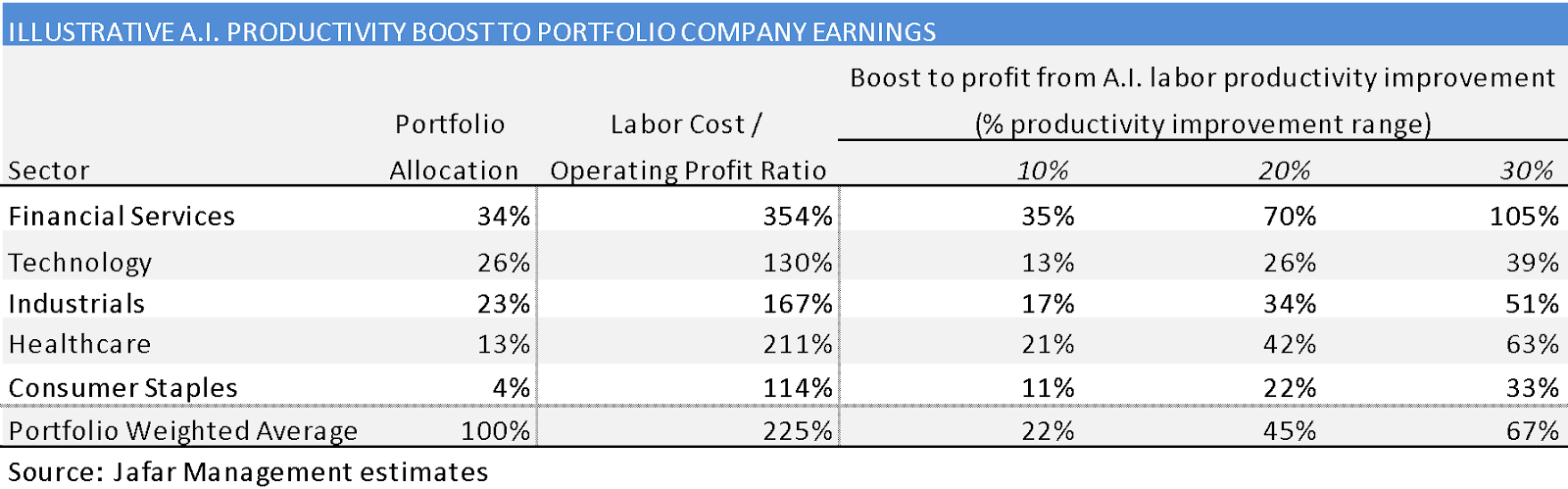

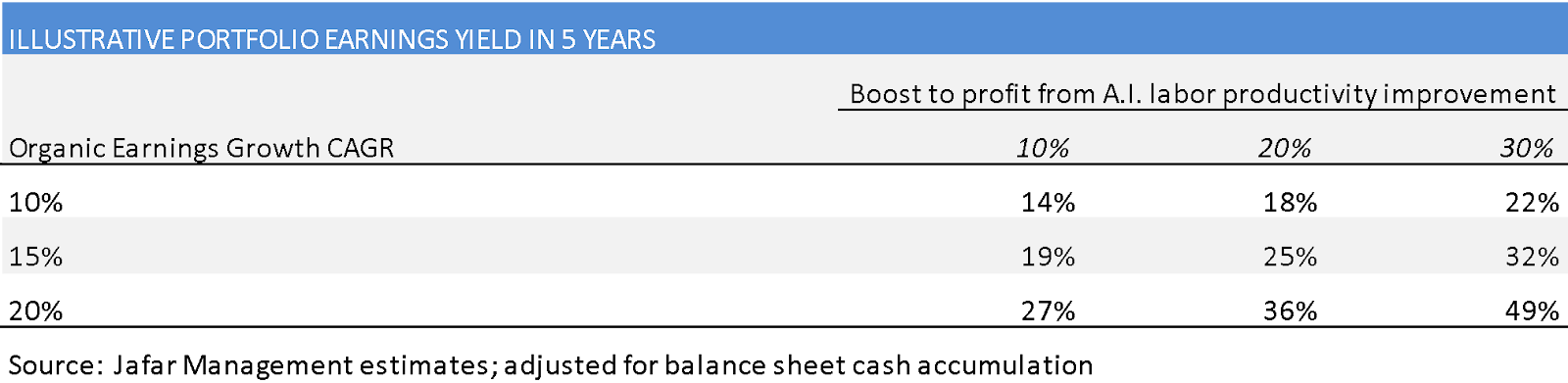

While last year’s hype regarding Artificial Intelligence (“A.I.”) brought attention to the Technology sector (~40% of the S&P 500 index), I believe the attention is misplaced. Given the very low barriers to creating the artificial intelligence products, it is my view that A.I. will be a commoditized, ubiquitous feature and not a true business model with any profit potential. Therefore, large incumbents across all sectors, with significant barriers to entry and monopolistic/oligopolistic industry structures stand to reap windfall profits as A.I. adoption proliferates. I have woven this theme across our entire portfolio, and while we are not counting on any A.I. benefits to generate returns (i.e. our investments are expected to generate multiples of money on a standalone basis, regardless of A.I.) the following tables provide context to the significant productivity potential from automation.

- The punchline: assuming +10-30% labor force productivity improvements, our portfolio earnings increase by +22-67% and the earnings yield in 5 years increases to +14%-49% from 5% today

Portfolio Update

During the summer and fall of 2023, mania around new weight-loss drugs (e.g. Ozempic, Wegovy, etc) spurred concerns that these “miracle” drugs would end obesity and reduce demand for food and health services. This fear led to panic selling of traditionally safe-haven stocks in the Consumer Staples and Healthcare sectors. My proprietary research and analysis which focused on the adoption curve of these drugs suggests the impact to food and healthcare demand is negligible (even in aggressive adoption scenarios). We took this opportunity to build stakes in Lamb Weston and HCA Healthcare for extraordinary earnings yields as high as +7.5% and +9%, respectively.

Lamb Weston (“LW”)

- LW is the #1 competitor in the North America Frozen Potato market (e.g. French fries, hashbrowns, etc) with 42% market share in an industry with an oligopoly market structure. Globally, LW has the 2nd largest market share. The attractive industry structure supports pricing power as evidenced by the company’s ability to increase profit margins despite the recent inflationary cycle

- Economically resilient, long-term demand growth of +2-4% (steady demand during the Great Financial Crisis 2007-2010)

- Consumer demand is very strong as evidenced by the fact that servings of French fries are 8x more than the next most popular appetizer or side dish

- Demand is supported by increased restaurant menu adoption because French fries are among the most profitable menu items for the restaurant (81% profit margins). Dominoes, Taco Bell and Starbucks have recently adopted fried potato products which is a testament to the consumer demand and highly profitable menu item

- I believe the Company’s pricing power and strong end market demand will enable LW to triple its earnings power over the next five years which supports several multiples-of-money return on our investment over that time horizon

HCA Health Care (“HCA”)

- HCA’s network of over 180 hospitals represents critical infrastructure for healthcare delivery in the United States

- HCA’s strong market share and national scale support the franchise’s pricing power

- HCA holds #1 or #2 market share positions across 81% of its geographic footprint with #3 share (and growing) in several others

- The Centers for Medicare & Medicaid Services project an acceleration in U.S. hospital demand of +6.1% per year from 2023-2029 (up from +5.2% between 2017-2023)

- A.I. is a significant opportunity

- HCA carries $42 billion of labor costs on top of its $13 billion of operating profit

- Nearly half the employee base does not provide medical care, and the Company has disclosed that medical professionals spend as much as 30% of their time on administrative tasks that can be automated

- HCA has partnered with Google to build a cloud-based infrastructure to support the networkwide rollout of its A.I. and data solutions. Early pilot programs started in December of 2023 with broader network adoption to occur over 2024 and beyond

- Given the robust demand growth and pricing power, I believe HCA will more than double its earnings power over the next five years. This base case scenario supports a multiple of money return on our investment. Should the benefits of A.I. materialize, I expect the returns to be significantly better than my base case

My family balance sheet remains fully invested in our partnership and I am excited about our future. It is a privilege to be at your service and I am honored by your partnership. Thank you for your trust and please feel free to reach out anytime.

Your partner and fiduciary,

Faris Jafar, Chief Executive Officer

Phone: (734) 678-8562